Not known Facts About Buying and Selling a Home in New Jersey - NJ.gov

Primary Residence Capital Gains Exclusion - Boring But Necessary - JVM Lending

Primary Residence Capital Gains Exclusion - Boring But Necessary - JVM LendingWhat Does Exclusion of Sleep Time from Hours Worked by Domestic Do?

Considering that the exclusion uses automatically to the first personality, a taxpayer would require to elect to be taxed on this one if it is the smaller sized of the 2. The guidelines define the term house fairly broadlyit consists of a houseboat, home trailer or stock held by a tenant-stockholder in a cooperative real estate corporation.

Home Exclusion - Metro Wildlife

Home Exclusion - Metro WildlifeAs a result, Certified public accountants must consult local law, especially on the status of mobile residences. If a taxpayer owns more than one home, practitioners will discover the decision regarding which house is the taxpayer's principal home depends upon all of the realities and scenarios. View Details say that the home a taxpayer uses for the majority of the time during the year will be considered his or her primary house for that year.

During each of these years, Albert lives in the Michigan house for seven months and in the Florida house for five months. If Albert chooses to offer among the houses in 2005, only the Michigan home will certify for the gain exclusion. Since he lives in Michigan for the majority of each year, that house is Albert's principal house for 2000 to 2004.

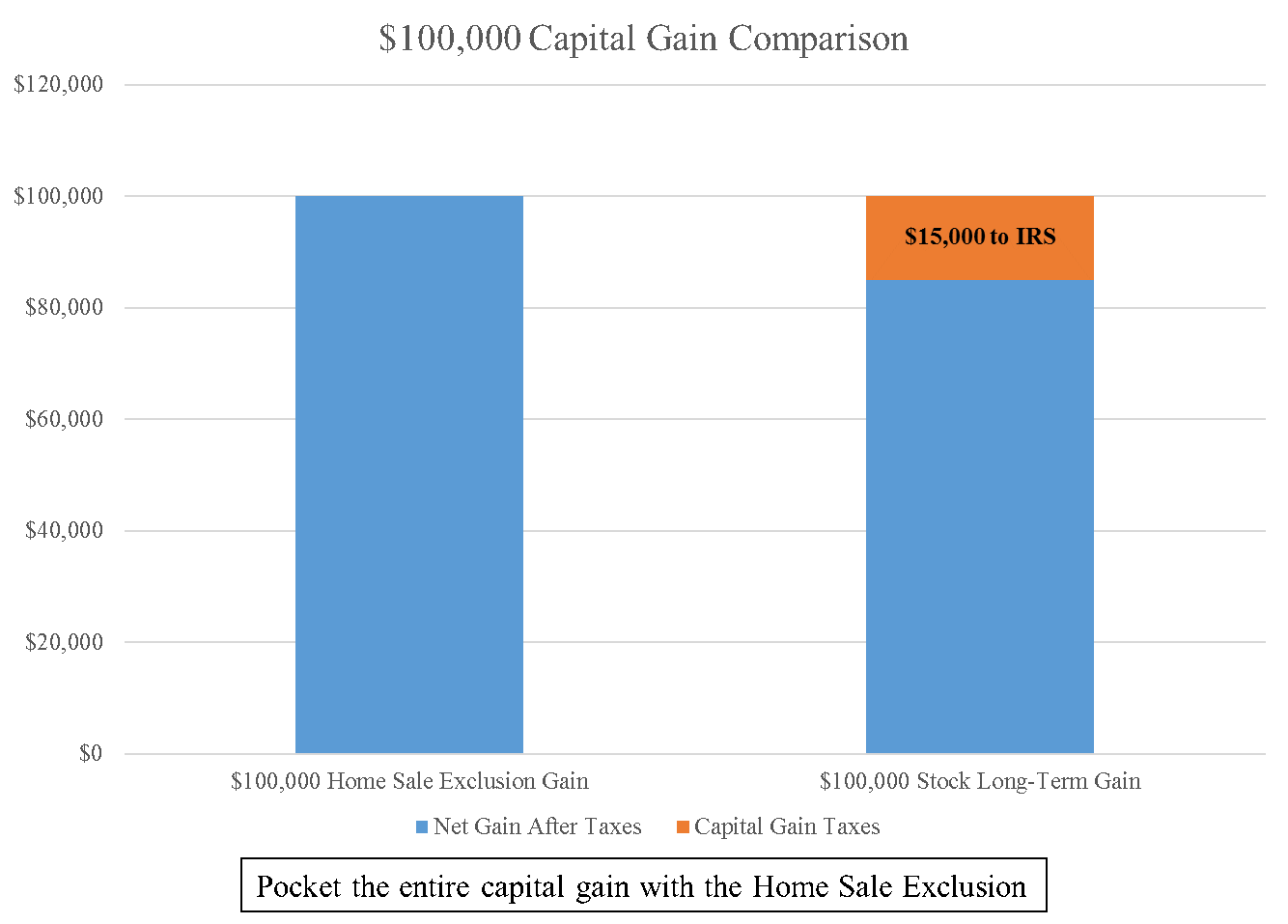

The gain on the sale of a house is left out from income just if, throughout that five-year duration, the taxpayer owns and utilizes the property as a primary residence for durations totaling 2 years or more. Either 24 complete months or 730 days will satisfy the two-year ownership and usage requirements.

The Home-Sale Gain Tax Exclusion - Hedley & Co CPA's Fundamentals Explained

On January 1, 2000 (24 months after purchasing the home), Barbara vacated town and started to rent the home. On December 28, 2002, she offers the property. Because Barbara owned and used the house as a primary residence for 24 months during the five-year period ending on the date of sale, she is qualified for the gain exclusion.

What is Capital Gains Partial Exclusion for Home Sale? 2021, 2022

What is Capital Gains Partial Exclusion for Home Sale? 2021, 2022In this case Barbara would not be qualified for the gain exemption because she would have resided in the house for just 23 months throughout the five-year period before the date of sale. The proposed regulations clarify that ownership and use durations do not need to be concurrent. Carmella rented a home from January 1, 1993 to January 1, 1998.