Facts About Guide to Securities: 4 Types of Financial Securities - 2022 Uncovered

Securities Finance November 2021 Snapshot - IHS Markit

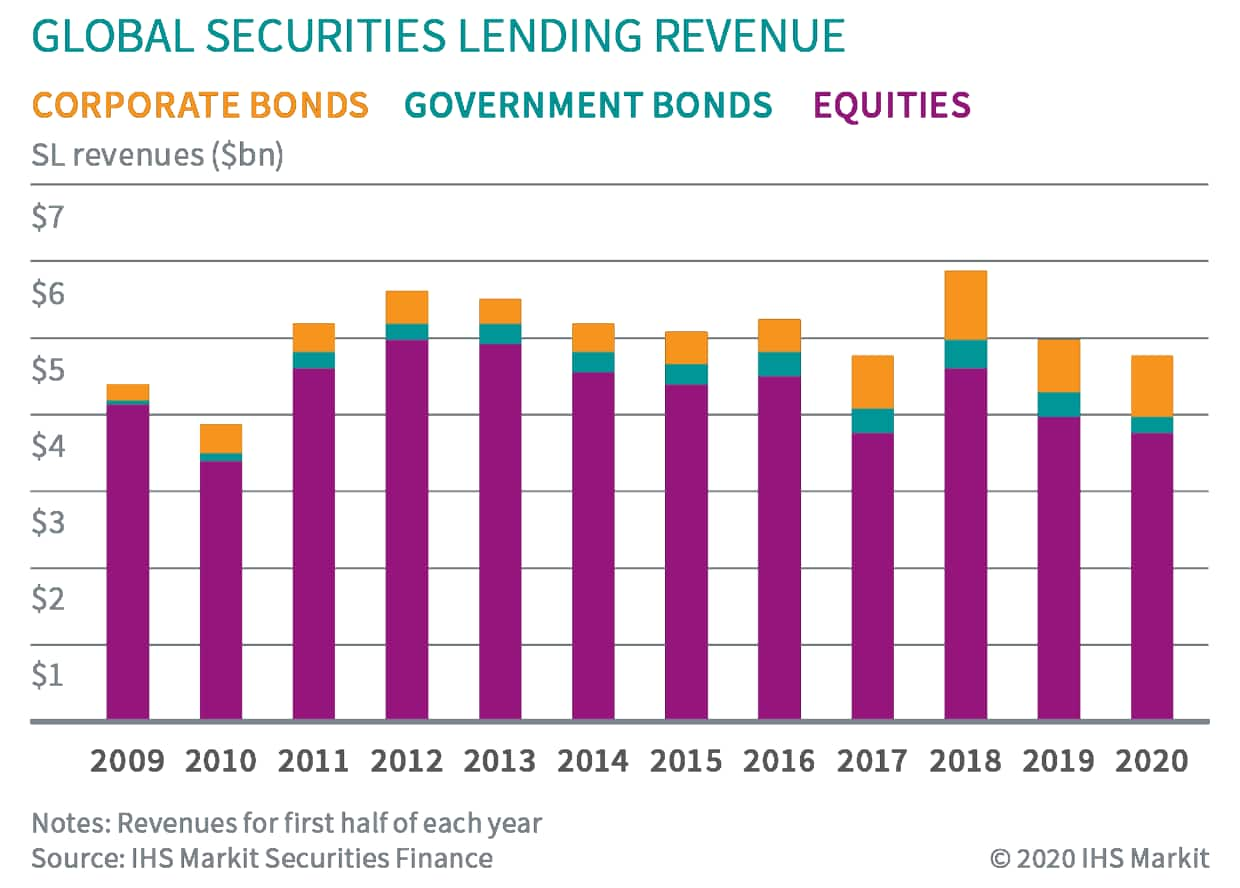

Securities Finance November 2021 Snapshot - IHS Markit SFM Magazine – Finadium

SFM Magazine – FinadiumYuanta Securities Finance Co., Ltd- Fitch Ratings Things To Know Before You Buy

Organized exchanges constitute the main secondary markets. Many smaller sized issues and many financial obligation securities trade in the decentralized, dealer-based non-prescription markets. In Europe, the primary trade company for securities dealers is the International Capital Market Association. In the U.S., the principal trade company for securities dealers is the Securities Industry and Financial Markets Association, which is the outcome of the merger of the Securities Industry Association and the Bond Market Association.

In India the comparable organisation is the securities exchange board of India (SEBI). Public deal and private positioning [modify] In the primary markets, securities might be provided to the public in a public deal. Additionally, they may be provided independently to a restricted number of qualified persons in a personal positioning.

The 4-Minute Rule for Home - Securities Finance Technology Symposium 2022

The distinction between the 2 is very important to securities policy and company law. Independently placed securities are not openly tradable and may only be purchased and sold by advanced qualified investors. As an outcome, the secondary market is not almost as liquid as it is for public (signed up) securities. Another category, sovereign bonds, is usually sold by auction to a specialized class of dealers.

Companies might look for listings for their securities to bring in investors, by making sure there is a liquid and regulated market that investors can buy and offer securities in. Development in informal electronic trading systems has actually challenged the conventional service of stock market. Large volumes of securities are likewise purchased and sold "nonprescription" (OTC).

TD Securities: Home - The Facts

There are likewise eurosecurities, which are securities that are released outside their domestic market into more than one jurisdiction. They are usually noted on the Luxembourg Stock Market or confessed to noting in London. The factors for listing eurobonds include regulatory and tax factors to consider, as well as the financial investment limitations.

The bank took part in securities services are generally called a custodian bank. Market gamers include BNY Mellon, J.P. Morgan, HSBC, Citi, BNP Paribas, Socit Gnrale and so on. Find Out More Here is the centre of the eurosecurities markets. There was a substantial increase in the eurosecurities market in London in the early 1980s. Settlement of sell eurosecurities is currently effected through 2 European digital clearing/depositories called Euroclear (in Belgium) and Clearstream (previously Cedelbank) in Luxembourg.